Spoiler alert: While local rents are on the rise, monthly mortgage payments are declining, despite the increased purchase prices! If you've been kicking yourself for not purchasing a home before prices surged, you can now congratulate yourself. Buying a home today could mean spending less on housing this year and saving a significant amount of money in the long run.

Many potential homebuyers are hesitating, concerned they might miss out on a future market correction or a slowdown in the frenzy of overpriced offers. Understandably, the steep price tags on homes play a significant role in shaping their perspective. In fact, despite rising rents, recent data shows a growing trend of people choosing to rent instead of buying a home.

As someone who values visual aids, I decided to delve into this question using a spreadsheet analysis. Assuming the terms of a conventional mortgage, specifically a 30-year fixed-rate mortgage with a 20% down payment, I compared the price of a home last year financed at available rates with the new price of the same home financed at today’s rates.

To my surprise, I discovered that mortgage payments would actually be lower now, even though home prices have surged. Here’s a breakdown of the analysis:

Imagine a quaint little yellow house you’ve had your eye on.

- It sold last year for $600K. With last year’s 4.55% average interest rate, the monthly loan payment came out to $2,447.

- Now, the same charming yellow house is priced at $720K. Financing it at today’s low rates means paying only $2,351 monthly, resulting in a monthly saving of $96.

- Over five years, that’s a total saving of $5,760. Moreover, if you keep your home for the life of the loan, the total interest paid decreases significantly from $400,694 to $270,529, a difference of $130,165.

Wow!

If you’ve been hesitating about buying a home, thinking you’ve missed the market, think again. You may have actually saved money by waiting. So, rather than dwelling on missed opportunities, take another look at that little house. You’ll be paying less to live in it today than you would have last year, and you’ll have saved a significant amount of cash over time. This might just be the perfect time to make your move into homeownership.

Numbers have been rounded up to the next whole integer. Monthly payments do not include tax and insurance.

FOR MOBILE DEVICES: This section is viewed best in landscape to see full table.

| YEAR | $ PRICE | $ LOAN | RATE | $ mo. | 30-yrs | ttl-int |

|---|---|---|---|---|---|---|

|

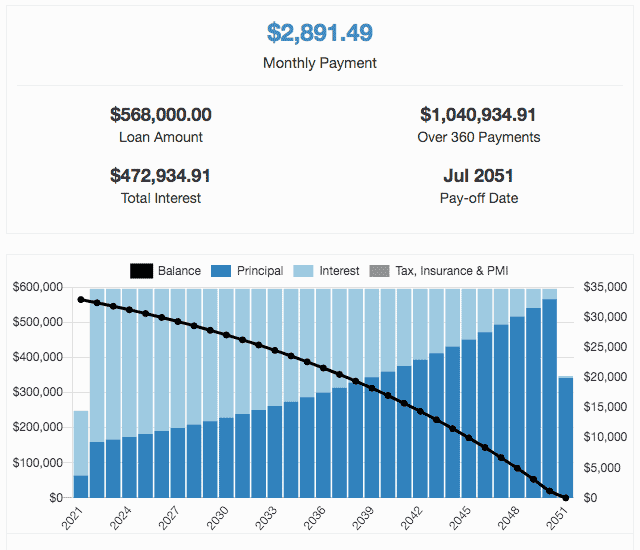

2018 |

$710,000 |

$568,000 |

4.54% |

$2,892 |

$1,040,935 |

$472,935 |

|

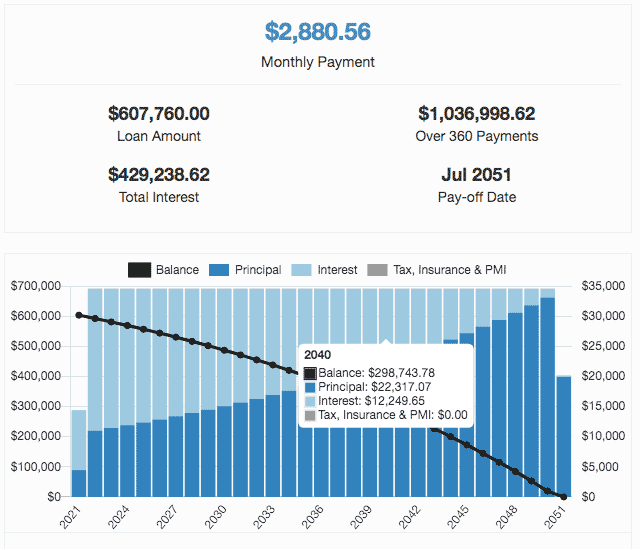

2019 |

$759,700 |

$607,760 |

3.94% |

$2,881 |

$1,036,999 |

$429,239 |

|

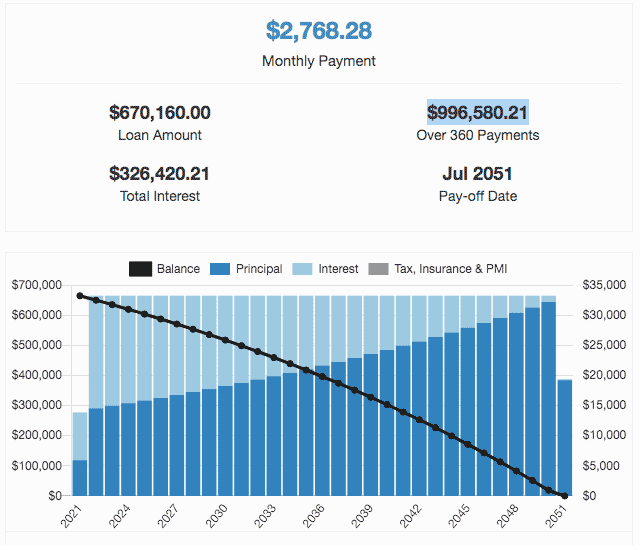

2021 |

$837,700 |

$670,160 |

2.84% |

$2,768 |

$ 996,581 |

$326,420 |

Important note: This scenario might be great for buyers who intend to live in the property for a while, but it may not be ideal for investors. The information presented is not meant to replace the advice of a financial planner.

Conclusion

The high purchase prices Southern California and many other areas in the United States are experiencing now may not be ideal for investors, regardless of the low interest rates available today. There is no crystal ball. Are prices going to continue to climb, or are we in a bubble destined to burst? No one wants to buy high and sell low as was the case several years ago.

However, if you find your ideal home and see yourself staying in it for a while, now may be the right time to buy. Your focus may be on how much cash you put out every month rather than short-term returns. When you secure a 30-year fixed-rate loan, it’s guaranteed that your monthly nut won’t get nuttier over time. If the market tanks in a few years, you may have time to wait it out before you sell. Rest assured that no matter what the market does, years from now your mortgage payments will be exactly the same as they would be if you purchase a home now with historically low interest rates—while rents continue to climb.

This article was written to give you some perspective on the current market, and maybe even provide you with some talking points for your next coffee meet-up with friends. It is not intended to replace the advice of your financial planner.

References

2021 Mortgage Property and Interest Payments

Note: In five years you are paying about 50/50 principal and interest.

2019 Mortgage Property and Interest Payments

Note: In five years you are paying more interest than principal.

2018 Mortgage Property and Interest Payments

Note: In five years you are paying 2/3 more interest than principal.